Recent research suggests this remodeling project will recoup more than its cost at resale.

10 Cities That Have Changed the Most

These U.S. metros have seen the most dramatic shifts in housing, incomes, crime rates, and economic foundations in the last decade, according to a...

Survey: Buyers Leery of Online Mortgage Info

Consumers trust real estate professionals and lenders more than online sources or family and friends to provide reliable guidance on obtaining a...

Battery-Powered Homes Are Becoming Reality

Municipalities in many states are revamping their electrical grids and turning to batteries to make them more efficient.

Remodeling Activity to Spike Through 2018

As homeowners gain more equity, they are expected to continue heavily investing in home improvement projects and repairs.

Empty Nesters Are Lured to Apartment Life

One of the biggest segments of new renters is seniors ages 55 and up, as multifamily developers reconsider their original focus on millennials.

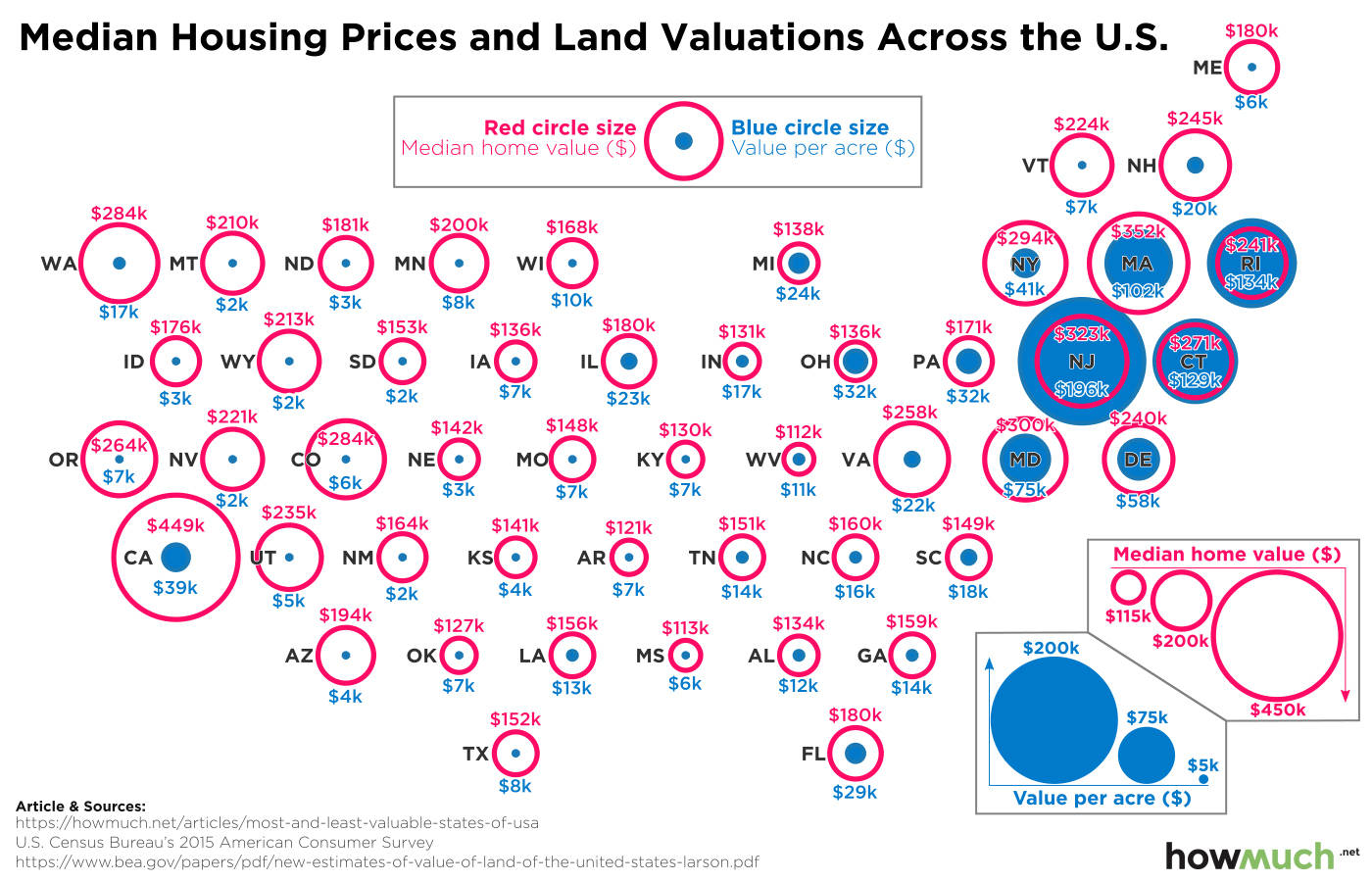

The Most (and Least) Valuable States in America

Editor’s Note: This was originally published on RISMedia’s blog, Housecall. See what else is cookin’ now at blog.rismedia.com:

- San Francisco: The Sweet Spot for Trick-or-Treaters

- Jeff Bezos May Seek HQ2 Close to Home

- Home Haunted? No Problem, New Survey Shows

Everyone knows location is the most important part of real estate. You can’t change where your house is (all things being equal). You have to consider school districts, crime rates, commute times—the list goes on and on. It can be much simpler when you’re considering buying a home to compare apples to apples so you can see how the real estate market differs according to location, so HowMuch.net created a new visualization showing land and housing prices at a glance.

The blue dots represent the value of an acre of land, and the red circles indicate the median value of a home. The bigger the blue dot and the larger the red circle, the more expensive it is to become a property owner. Small circles and dots likewise indicate a very low cost of purchasing property. The home values are from the U.S. Census Bureau’s 2015 American Consumer Survey, and the numbers behind the land values come from the Bureau of Economic Analysis.

Several things stand out in the illustration. An acre of land is much more valuable in the Northeast compared to any other part of the country. This is partly because the Eastern seaboard is a very densely populated area with several large cities, most notably New York. New York and Massachusetts have some of the oldest modern structures anywhere in the U.S. In other words, Eastern cities are a lot older than Midwestern cities, so there isn’t a lot of farmland for suburban expansion anymore. In terms of geographic size, these are some of the smallest states in the country. As a matter of fact, the three states where the cost of an acre of land is greater than the median price of a house are all located on the East Coast, and they happen to be some of the smallest states in the Union (Rhode Island, Connecticut, and New Jersey).

Median home values (the red circles) are a different and more complicated story. California has the most expensive houses by far ($449,100). Oregon and Washington boast similarly high housing valuations, as well ($264,100 and $284,000, respectively). It is also expensive to buy a home on the East Coast, with six out of the top 10 states with the most expensive median home values.

There’s a noticeable dip in both housing and land prices in Southern and Midwestern states. Prices slowly rise the further you move from east to west. This highlights unique economic developments over the last several years, including the boom in oil exploration in North Dakota and the growth of Western cities, like Denver, thanks to young people. Snowbirds also tend to move to Florida and Arizona when they retire, which also pushes up housing prices in those places.

Top 5 Most Expensive States to Buy a Home

- California

Value per Acre: $39,092

Median Home Value: $449,100

- Massachusetts

Value per Acre: $102,214

Median Home Value: $352,100

- New Jersey

Value per Acre: $196,410

Median Home Value: $322,600

- Maryland

Value per Acre: $75,429

Median Home Value: $299,800

- New York

Value per Acre: $41,314

Median Home Value: $293,500

Top 5 Cheapest States to Buy a Home

- West Virginia

Value per Acre: $10,537

Median Home Value: $112,100

- Mississippi

Value per Acre: $5,565

Median Home Value: $112,700

- Arkansas

Value per Acre: $6,739

Median Home Value: $120,700

- Oklahoma

Value per Acre: $7,364

Median Home Value: $126,800

- Kentucky

Value per Acre: $7,209

Median Home Value: $130,000

All this shows that the laws of supply and demand are alive and well in the real estate market. You can easily find cheap acres of land where they are plentiful and un-useful (sorry, Nevada), but owning property is a lot more expensive in smaller places crowded with lots of people. As always: location, location, location.

A version of this article originally appeared on HowMuch.net.

For the latest real estate news and trends, bookmark RISMedia.com.

The post The Most (and Least) Valuable States in America appeared first on RISMedia.

Appraisal Disappointing? Steps to Take

Appraisal disappointing? You have options, according to the Appraisal Institute.

“Homebuyers and sellers should first understand what an appraisal is and how it’s used,” says Jim Amorin, president and acting CEO of the Appraisal Institute. “Real estate appraisals for mortgage finance applications are prepared for the bank or financial institution so they can better understand the collateral risk in making the loan. This can be confusing, because homebuyers typically pay for the appraisal and receive a copy of it.”

In some cases, the appraisal may not match the contract price—but just because an appraisal comes in below (or above) the listing or contract price doesn’t mean it’s flawed, Amorin says. The agreed-upon contract price may be above market value, for example. In those situations, the buyer and seller often renegotiate the contract at more favorable or balanced terms.

Homebuyers should ask their lender for the qualifications of the appraiser, including whether they are designated by a professional association like the Appraisal Institute, says Amorin. A qualified and competent appraiser knows how to conduct a thorough market analysis and make appropriate adjustments.

Homebuyers also can ask whether the appraiser is directly engaged by the bank or whether the bank utilizes an appraisal management company, and what their procedures are for engaging qualified appraisers.

“The best way for consumers to combat potential problems with appraisals is to ensure the appraiser hired by their lender is highly qualified and competent,” Amorin says. “Consumers have every right to demand the use of a highly qualified appraiser, someone with field experience in their market and knowledge and experience to handle the assignment properly.”

Contrary to incorrect interpretations of appraiser independence requirements, appraisers welcome information that would assist the development of credible assignment results,” says Amorin. If lender policies permit, consumers can accompany appraisers when conducting the property inspection and may provide the appraiser with any information they consider important.

Amorin suggests consumers ask their lender for permission to do so, and confirm the appointment. Consumers should also take note of whether an adequate inspection is performed. Did the appraiser spend enough time at the property to observe important features or improvements or potential problems?

Homebuyers should take advantage of their right to obtain a copy of the appraisal report,” Amorin says. Even though the appraisal is ordered to help assess lender collateral risk, buyers are entitled to a copy of the appraisal report. Federal regulations require lenders to provide property buyers with free copies of appraisal reports no later than three days before the loan closes.

Although appraisal review is best performed by qualified appraisers, consumers should examine the appraisal for potential deficiencies, says Amorin. According to “Appraising the Appraisal: The Art of Appraisal Review,” common errors in appraisals include: misuse of adjustments to comparables; disregarding special financing and concessions; or miscalculation of gross living area (GLA).

Amorin suggests consumers ask themselves:

- Do adjacent homes add or detract from the value of the subject property?

- Is the subject property equal to or lower in price than surrounding homes?

- Does the floor plan have any functional problems?

- Does the house (particularly the kitchen and bathrooms) require major remodeling to make it comparable with similar homes in the same price range?

- Is the number of bedrooms and baths in the home comparable to similar homes in the same price range?

- Did the appraiser perform an adequate inspection?

“Most lenders have appraisal appeal procedures, known as ‘Reconsiderations of Value,'” says Amorin. “If you’re aware of recent, comparable sales information or items that may not have been available or considered by the appraiser, provide those to the lender. If problems were found with the first appraisal, you can and should obtain a second appraisal.”

Source: Appraisal Institute

For the latest real estate news and trends, bookmark RISMedia.com.

The post Appraisal Disappointing? Steps to Take appeared first on RISMedia.

Meager Sales Rebound Underscores Tough Market

Real estate transactions remain near their lowest level of the year, despite buyer interest in most parts of the country, NAR reports.

Can Developers Please Both Boomers and Millennials?

The two generations don’t always agree on what they want in a home, posing challenges for builders who are striving to meet both groups...